Spring has sprung and with it, the risk of wildfires. If you think devastating wildfires only happen in places like California and the Southwest, think again. Case in point: watching Lahaina go up in flames several years ago was surreal precisely because it was so out of the ordinary. We don’t normally think of Hawaii as a wildfire hot spot. But that’s the point. As our climate continues to feel the effects of ever-increasing droughts and rising temps, we are starting to see places burn that never did before. Here’s how wildfire risks affect real estate and what to do about it:

At the time the Maui fire broke out in 2023 twenty percent of the island was in drought. Overdevelopment and water management challenges exacerbated the problem by reducing the availability of water needed to put out the fire. Likewise, when the Jennings Fire broke out between New Jersey and New York City in October of 2024 drought and abnormally dry conditions set the stage for fire. It was the largest wildfire those areas had seen in decades, burning roughly 5000 acres between the two states.

What is particularly problematic about wildfires in places we don’t expect them is that most of these areas have higher population densities, more abundant fuel and are less prepared. These areas also usually receive more rainfall than dry areas like California and the Southwest, with the assumption that greener areas won’t burn. But as drought and higher temps create what is known as “flash drought” wildfire risk in these green areas has become an ever-increasing eventuality. As such, wildfire risk has extended well beyond California and the Southwest and is becoming part of a “new normal.” As the likelihood of wildfire expands its boundaries into more states across the map it threatens property values and the ability to secure fire insurance across the country. This has become a real problem when it comes to real estate transactions and is responsible for many deal cancellations once buyers discover how much insurance will cost.

WILDFIRES VS URBAN WILDFIRES

A wildfire is defined as “an unplanned, uncontrolled fire burning in natural vegetation such as forests, grasslands or prairies.” These fires are often started by lightning or human negligence and can spread rapidly. They consume vast areas and pose threats to ecosystems, wildlife, and human communities.

However the definition of wildfires is morphing into a much more sinister reality as we continue to experience the negative effects of climate change. This new reality is being coined the Age of the Pyrocene. As you may have noticed, recent wildfires are no longer keeping to themselves in “wild” areas. More and more we are seeing wildfires spread into highly populated “city” areas.

A USA TODAY analysis found that 3.3 million Americans live in census tracts where the wildfire risk is “very high” (California and the Southwest). Another 14.8 million live in tracts where the risk is “relatively high” like Texas, New Jersey, Oklahoma City, Nevada, Idaho, and Utah. But don’t stop there. States that have historically been considered “low risk,” like Tennessee, Kentucky, West Virginia and the Carolinas all have areas with the potential for large urban wildfire events. Examples of what’s to come include the 2016 Gatlinburg Wildfires in Tennessee and the 2024 Smokehouse Creek Fire in Texas and Oklahoma. Not surprisingly California tops the list with the 2017 Tubbs Fire which destroyed 1300 homes and evacuated tens of thousands of people with very little notice. And two years later the Kincaide Fire which threatened over 90,000 structures and caused widespread evacuations throughout Sonoma County. And again, in January of 2025 the infamous Eaton and Palisades Fires burned through the densely populated, expensive neighborhoods of Malibu, Topanga, Altadena and Pacific Palisades. All of these wildfires started in “wilderness areas” but then quickly spread into highly populated towns and neighborhoods. Experts predict the recent phenomenon of “urban wildfires” is becoming the “new normal.” Why? Population growth, climate change and the fact that people still want to live in “natural” areas has blurred the boundaries between wild areas and populated areas. (See wildfire statistics by state.)

WILDFIRES, PROPERTY VALUES AND INSURANCE

Urban wildfires are creating a perfect storm for property values and the ability to obtain fire insurance. A number of insurance companies have quit writing policies altogether in states like California, Texas and Florida. And even though state-mandated FAIR plans offer a last-resort insurance option the coverage is drastically expensive and offers limited coverage. As such, homes in high fire zones have seen values decline due to insurance and affordability problems centered around fire risk.

MINIMIZING RISK

Homeowners can minimize wildfire risk (and possibly insurance costs) by creating defensible space and “hardening” their homes against ember intrusion. Key actions include:

- Removing vegetation 5 feet from structures

- Cleaning roofs and gutters

- Installing ember-resistant vents (1/8-inch mesh)

- Using Class A fire-rated roofing

- Replacing combustible materials near the home with gravel or stone

See: How to Make Sure Your Deal Survives Homeowner’s Insurance

INSURANCE SOLUTIONS

Working with your insurance company is another must as wildfire risks grow. Insurance is an essential tool for providing financial protection after a disaster. As insurance rates climb ever higher they are helping to shape consumer behavior, such as incentivizing building and landscape upgrades that make homes more resistant to wildfire.

While there is no single solution insurance strategies can play a role in reducing damages and guiding homeowners to be more responsible about mitigating wildfire hazards. Investing in community-driven wildfire resistant construction, vegetation maintenance and neighborhood planning can minimize wildfire damage and make insurance more accessible.

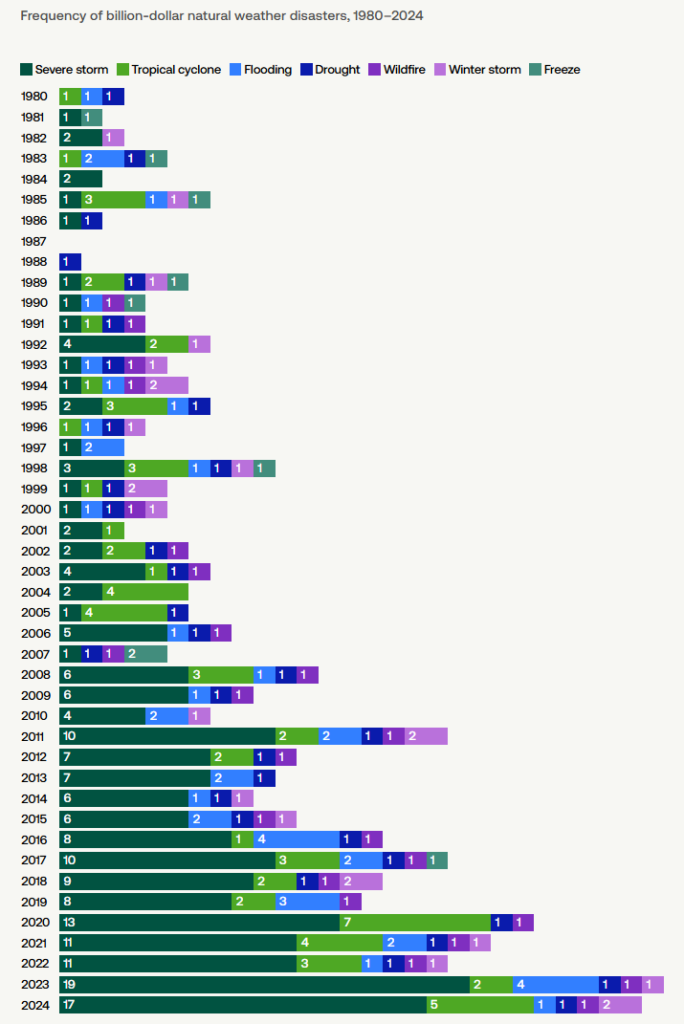

Finally, finding solutions via state legislature targeted at state-mandated insurance regulations are more important than ever. Billion-dollar disasters have risen from an average of nine per year (since 1980) to over 20 annually in recent years, driven by climate change, increased infrastructure exposure, and development in high-risk coastal and fire-prone areas.

Currently property insurance is a state-based system with limited federal oversight, focused heavily on market stability rather than day-to-day rate setting. But as climate-related natural hazards become more frequent and expensive it seems likely that all levels of government will need to work together to create solutions that safeguard homes and, by extension, the American Dream itself.

ATTENTION CALIFORNIA

In California, sellers are legally required to provide a Natural Hazard Report to buyers outlining risks like floods, wildfires and earthquakes. These reports identify if a property is in a designated high-risk area (e.g., fault zones, fire hazard severity zones).

- Timing: The NHD is typically provided early in the escrow process to inform the buyer’s decision.

- Liability: Failure to provide a proper NHD report can make the seller liable for damages.

- Insurance: These reports help determine if a home requires specific, often costly, hazard insurance, such as flood or specialized fire insurance.

Learn more about Disclosure Source, the real estate industry’s premier provider of natural hazards, tax and environmental information for the State of California.

Options for Insurance Coverage

See: How to Make Sure Your Deal Survives Homeowner’s Insurance